Published on Richard Evans’ Econosseur substack.

Will AI be the accelerant of broad-based wealth concentration in the hands of a few? Economic theory and economic data tell us that the answer is a resounding… “probably not”.

Wealth inequality had a moment back in 2014 with the publication of Piketty’s landmark book, Capital in the Twenty-First Century. Now the distribution wealth is having another smaller moment corresponding to increased worries by some about the progress and proliferation of AI. The questions from a decade ago are the same ones we are asking now. Can wealth inequality grow indefinitely? And will AI be the accelerant of broad-based wealth concentration in the hands of a few? Economic theory and economic data tell us that the answer is a resounding… “probably not”.

It is actually a comforting credibility of economics that most of its answers are not an absolute yes or absolute no. Instead, economics balances the costs with the benefits and weighs multiple kinds of evidence to arrive at a probability or what is usually something between yes and no.1

In this article, I provide evidence from economic theory and economic historical data that extreme wealth concentration is unlikely to result from the progress of AI. I start with a summary and context of some recent comments from economists, AI practitioners, and media about their forecasts and justifications for how they think AI will influence the future of wealth inequality.

I then summarize a 2019 paper of mine that tests the central hypothesis of Thomas Piketty (2014) that wealth inequality can grow without bound. Our answer is that only in rare and unlikely cases can wealth inequality grow indefinitely.

I conclude by presenting two economic principles that are taught in every introductory economics course that each provide natural offsetting forces to potential imbalances caused by AI-induced wealth inequality: (i) prices adjust to counteract imbalances in supply and demand, and (ii) labor and capital are almost always complements.

Current Debate

To close out the year in 2025, Philip Trammell and Dwarkesh Patel published a Substack article entitled, “Capital in the 22nd Century”.2 Their title makes clear that they are commenting on and updating the empirical and theoretical predictions of Thomas Piketty’s (2014) much cited, Capital in the Twenty-First Century.

Piketty’s main thesis is that wealth inequality can grow without bound when the rate of return on capital exceeds the economic growth rate, when some individuals save more than others, or when some individuals receive higher returns on investment than others.

When the rate of return on capital significantly exceeds the growth rate of the economy (as it did through much of history until the nineteenth century and as is likely to be the case again in the twenty-first century), then it logically follows that inherited wealth grows faster than output and income. People with inherited wealth need save only a portion of their income from capital to see that capital grows more quickly than the economy as a whole. Under such conditions, it is almost inevitable that inherited wealth will dominate wealth amassed from a lifetime’s labor by a wide margin, and the concentration of capital will attain extremely high levels—levels potentially incompatible with the meritocratic values and principles of social justice fundamental to modern democratic societies. (Piketty, 2014, p. 26)

Trammell and Patel start with a critique of Piketty, that his interpretations of the 20th century and the resulting predictions for the 21th century are too strong because he neglects the importance of labor’s complementarity with capital.3 But Trammell and Patel’s main thesis is that Piketty’s prediction of unbounded growth in wealth inequality is more likely in a society in which the productive process is dominated by capital—robotics run by AI.

It is true that if… AI and robotics push human labor out of the production process…, then wealth inequality can grow without bound. But…labor and capital have empirically been… complements, especially in times of rapid advancements in capital technology. In other words, when capital’s capability advances, humans tend to find ways to make their productivity advance and catch up.

The key assumption and prediction in this argument is whether labor will continue to be important in the production process when AI and robotics become more capable than humans for many tasks. It is true that if capital exemplified by AI and robotics push human labor out of the production process (labor and capital are gross substitutes), then wealth inequality can grow without bound—a result with clear theoretical support to which I will refer in the next section.

But I will provide evidence in this section and in the last section of this article that labor and capital have empirically been gross complements, especially in times of rapid advancements in capital technology. In other words, when capital’s capability advances, humans tend to find ways to make their productivity advance and catch up.

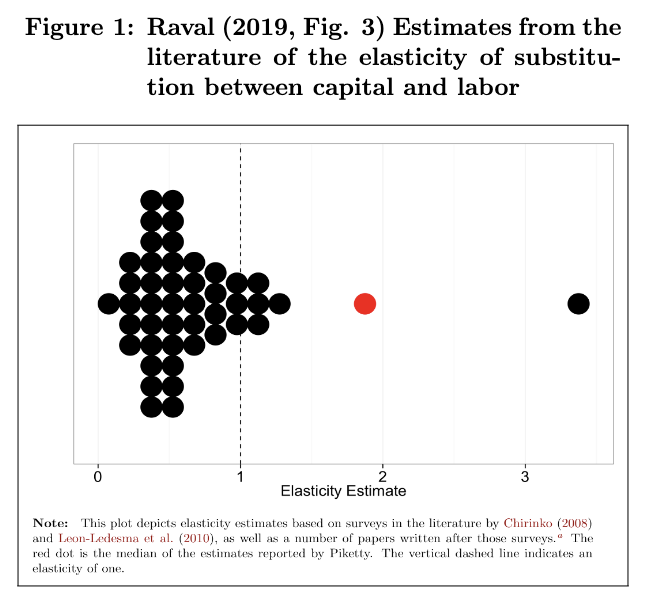

Brian Albrecht had a nice response article to Trammell and Dwarkesh as well as some insightful interactions on social media.4 One of the most salient pieces of evidence from Albrecht’s article is his reference to U.S. Federal Trade Commission report from 2019 that gives a visual representation of a survey of estimates from the literature of the elasticity of substitution between capital and labor.

Note that the vast majority of empirical estimates of the elasticity of substitution between capital and labor are less than one. This means that for most of the estimates of this parameter in the 20th and 21st centuries, labor and capital have been found to be gross complements (a low elasticity of substitution). As Piketty, Trammell and Patel, and Albrecht all recognize, it is the counterfactual relationship of labor and capital being substitutes that is a necessary condition for wealth inequality to grow without bound.

Economic Theory: Natural Limits to Increasing Wealth Inequality

We find that all the standard hypothesized causes of wealth inequality do actually increase wealth inequality. But only in the rarest and least empirically plausible cases can wealth inequality grow without bound.

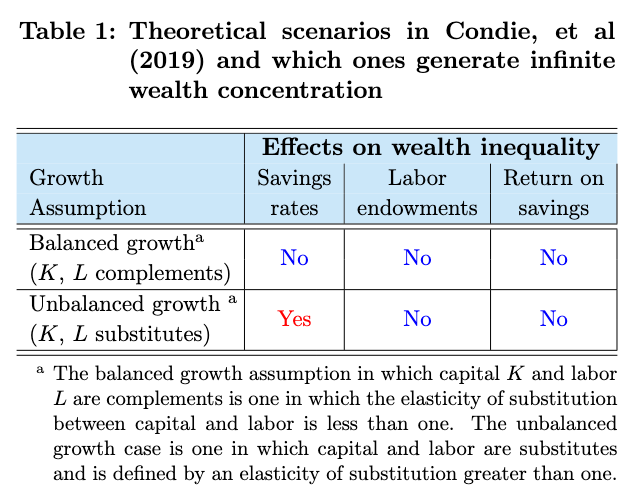

Scott Condie, Kerk Phillips, and I published a paper in 2019 entitled, “Natural Limits of Wealth Inequality and the Effectiveness of Tax Policy.” In this paper, we tried to answer how likely it is for the wealth distribution to grow without bound. We did this by studying how the wealth distribution evolves over time in an economic model that has all the key characteristics that you would expect to matter. We then tested whether the most common explanations for causes of growth in wealth inequality resulted in indefinite increases in wealth inequality in the model.

A summary of our findings is that all the standard hypothesized causes of wealth inequality do actually increase wealth inequality. But only in the rarest and least empirically plausible cases can wealth inequality grow without bound. Hence, my answer of “probably not” to the question of whether AI will cause wealth inequality to grow without bound.

We wrote this paper as a response to Piketty’s (2014) main thesis that I have cited above. And the results of our paper are relevant to the current question of how AI will influence the growth of wealth inequality.

The laboratory for our experiments was an economic model that had all the salient component for a question of how the distribution of wealth would change over time. The model was general equilibrium so that prices adjust to offset imbalances in supply and demand. We represented individuals in the model as overlapping dynasties who pass wealth from one generation to the next in order to capture the most important characteristics of how wealth is accumulated over time.

As shown across the columns of Table 1 we tested whether wealth inequality could increase indefinitely under three main scenarios, each of which is listed in the literature as the most likely causes of disparities in wealth: (i) individuals saving at different rates, (ii) individuals having different labor endowments or labor productivity, and (iii) individuals earning different rates of return on their savings.

We studied these three potential causes of wealth inequality under two different assumptions about the elasticity of substitution between capital and labor. The two rows of Table 1 show the results for the case in which capital and labor are gross complements (the most empirically plausible) and the results for the case in which capital and labor are gross substitutes.

Our results, summarized in Table 1, were that none of the drivers of wealth inequality resulted in perpetually increasing inequality in an economy in which capital and labor are gross complements. And under the much stronger assumption that capital and labor are gross substitutes, only differences in savings rates among individuals could generate ever increasing wealth inequality.

Two Basic Economic Principles

(1) Prices adjust until supply equals demand. (2) Labor and capital have been complements throughout history. These two principles provide intellectual guardrails against many extreme economic predictions.

1. Prices adjust until supply equals demand

One of the first principles of economics is that supply equals demand. Put more carefully, prices adjust until supply equals demand. This is fundamentally a general equilibrium argument. That is, it requires a model of both the supply side and demand sides of an economy. Then prices are determined that set supply equal to demand. This differs from partial equilibrium analysis in which prices are taken as given and one studies either the supply or demand of an economy or individual separately.

This principle of prices adjusting to offset imbalances in supply and demand is the key intellectual framework for understanding the large costs imposed by governments implementing price controls, like minimum wage, rent control, drug price limits, tariffs, quotas, etc.

This mechanism of price equilibrating supply and demand also helps dispell extreme economic predictions. The end of the 1990s and early 2000s saw a swell of articles and papers suggesting that the earth was going to run out of petroleum fossil fuel. These arguments were collectively labeled “peak oil.”5 What these thought leaders did not account for was that oil prices would rise as supply became scarce, thereby rationing the consumption, and that substitute energy use applications like EVs and renewable generation would expand in response. The extreme predictions of peak oil were never realized. And the simple principle of prices adjusting to equilibrate supply and demand could have prevented these arguments from gaining credibility.

This principle also applies to discussions of AI and capital and labor. As AI applications replace the functions and positions of humans in businesses, a key step in the heirarchy progression is broken. The entry step to middle- and upper-management is diminished, and the price for those skills and those individuals will increase. Worker wages will rise to increase labor supply and decrease labor demand. A lot more work will be done on the effects of AI on the interaction between capital and labor.

2. Capital and labor have always been complements

With the exception of short episodes, primarily restricted to particular industries, capital and labor have always been complements. And the thesis of Trammell and Patel, which I pose as a sequence of questions, is the following. Will the progress of AI and robotics evenutally force human labor out of the productive process? And will AI be the accelerant of broad-based wealth concentration in the hands of a few?

If the answer to the first question is yes, then the answer to the second question is yes. If capital and labor are substitutes and AI pushes human labor out of the production process, then wealth inequality can expand indefinitely. The Condie, et al (2019) study further qualifies that this is only true if capital and labor are substitutes and if individuals have different savings rates (see row 2 of Table 1).

But I argue that this scenario is highly unlikely. Labor and capital have been complements over all of recorded history if you limit yourself to economy-wide estimates over time periods that are not too short.

We’ve already seen in Figure 1 from Raval (2019, Fig. 3) that the vast majority of estimates of the elasticity of substitution between capital and labor suggests that they are complements. One proposed counterexample is that capital and labor were substitutes in Britain in the Industrial Revolution, when capital broadly replaced labor. Another proposed counterexample is the US post-1980 automation and IT revolution. However, Acemoglu and Restrepo (2019) point out that this was task substitution not factor substitution in the production function sense. In lay terms, the Industrial Revolution and Internet revolution created sectoral shifts and changed the types of tasks labor performed, rather than replacing labor.

Bringing this principle back to artificial intelligence, this principle is the reason why I predict that AI will augment labor’s productivity rather than replace it. In every other technological advancement of the last 150 years—of which there have been many—increases in capital productivity were quickly followed by increases in labor productivity. With AI, I see the technology increasing my own productivity every day. I look forward to the day in the not too distant future when education is customized and administered by expert teachers managing AI agents to a larger number of students learning in the way that is optimized for them.

All evidence points to AI and robotics augmenting the value of our human labor rather than replacing it. The valid fear expressed by Trammell and Patel has also been a natural and consistent response of many over the last 150 years to every new technology.6 But history and economic theory tell us that human labor has the potential and likelihood to benefit greatly from AI progress.

References

Acemoglu, Daron and Pascual Restrepo, “Automation and New Tasks: How Technology Displaces and Reinstates Labor,” Journal of Economic Perspectives, 33:2, pp. 3–30 (2019).

Acemoglu, Daron and J. Robinson, “The Rise and Decline of General Laws of Capitalism,” Journal of Economic Perspectives (2015).

Albrecht, Brian, “Will AI Prove Piketty Right?,” Substack post (Jan. 9, 2026).

Appenzeller, Tim, “The End of Cheap Oil,” National Geographic (Jun. 2004).

Bakhtiari, A.M.S., “World Oil Production Capacity Model Suggests Output Peak by 2006–07,” Oil & Gas Journal (Apr. 26, 2004).

Bardi, Ugo, “Peak Oil, 20 Years Later: Failed Prediction or Useful Insight?” Energy Research & Social Science, (2019).

Campbell, Colin J., Jean H. Laherrère, “The End of Cheap Oil,” Scientific American, 278:3, pp. 78-83 (1998).

Carroll, C., J. Slacalek, K. Tokuoka, and M. White, “The Distribution of Wealth and the MPC”. Quantitative Economics (2017).

Condie, Scott S., Richard W. Evans, and Kerk L. Phillips, “Natural Limits of Wealth Inequality and the Effectiveness of Tax Policy,” Public Finance Review, 47:1, pp. 32-57 (Jan. 2019).

Deffeyes, Kenneth S., Hubbert’s Peak: The Impending World Oil Shortage, Princeton University Press (2001).

Goldin, C. and L. Katz, The Race Between Education and Technology (2008).

Hirsch, Robert L., Roger Bezdek, and Robert Wendling, “Peaking of World Oil Production: Impacts, Mitigation, and Risk Management,” Hirsch Report, Department of Energy (2005).

Jones, T.H., “A Critique of Hubbert’s Model for Peak Oil,” FACETS Journal (2018).

Kaplan, S., and J. Rauh, “Wall Street and Main Street: What Contributes to the Rise in the Highest Incomes?” Review of Financial Studies (2010).

Mankiw, N. G., “Yes, r > g. So What?” American Economic Review Papers & Proceedings (2015).

Piketty, Thomas, Capital in the Twenty-First Century, translated by Arthur Goldhammer, The Belknap Press of Harvard University Press, 2014.

Raval, Devesh, “Whats Wrong with Capital in the Twenty-First Century’s Model?” Federal Trade Commission (Apr. 13, 2019).

Rognlie, Matthew, “Deciphering the Fall and Rise in the Net Capital Share”. Brookings Papers on Economic Activity (2015).

Solow, Robert, “Thomas Piketty Is Right… But”. The New Republic (2014).

Trammell, Philip and Dwarkesh Patel, “Capital in the 22nd Century,” Substack post (Dec. 30, 2026).

1 In the mathematical terminology of optimization, this principle is referred to as an interior solution. Most point estimates or optima of a maximization problem are not at the boundaries or constraints of the problem. They most often lie in the interior of the set of possibilities.

2 Philip Trammell is an economics postdoc at Stanford University’s Digital Economy Lab. And Dwarkesh Patel is an AI, science, and history author and podcaster.

3 A large literature responded to Piketty (2014), levying criticisms and providing validation. My summary of the mainstream economics consensus opinion of Piketty (2014) is that he provided compelling data collection and description of the distribution of wealth across many years and many economies. There are questions about his definitions of capital, his interpretation of theory, and his policy prescriptions. But the work represented a large step forward in our understanding of and questions about the distribution of wealth. See Acemoglu and Robinson (2015), Solow (2014), Ronglie (2015), Carroll, et al (2017), Mankiw (2015), Kaplan and Rauh (2010), Goldin and Katz (2008).

4 Brian Albrecht is Chief Economist at the International Center for Law & Economics. For references to insightful threads on social media, see this Jan. 6, 20206 post on X, and this Dec. 30, 2025 post on X.

5 See Campbell and Laherrère (1998), Deffeyes (2001), Hirch, et al (2005), Bakhtiari (2004), Appenzeller (2004). See Bardi (2019) and Jones (2018) for ex post critiques of why the peak oil arguments were wrong.

6 See The Pessimists Archive, curated by Louis Anslow.