Published by The Beacon Center of Tennessee. Read the full paper here.

This report was co-authored by Jason Edmonds, Director of Policy at The Beacon Center of Tennessee.

Reliable energy has been the engine of American progress. But as the country has become more prosperous, technologically advanced, and populous, energy demand has gone from a concern to a national priority. Few states feel these pressures more than Tennessee. Since 2010, Tennessee’s population has grown by 16 percent, from 6.3 million to 7.3 million people. [1] By 2040, the state’s population could be eight million, according to the University of Tennessee. [2]

As the population grows, so does the state’s economy. According to a recent Tennessee Department of Labor and Workforce Development report, economic growth has remained healthy in recent years, and the authors project that by 2032, manufacturing jobs will be the second largest sector in total jobs added. [3] As it happens, this is the very sector that demands the most electricity and energy. Tennessee must generate more power to continue its encouraging economic trajectory.

Fortunately, technology can meet all these energy needs if policy frameworks permit.[5] Progress in advanced nuclear energy generation, particularly small modular reactors (SMRs), is among the most promising approaches. The deployment of SMRs is not merely about increasing supply; it represents a strategic solution to modern energy challenges. SMRs provide around-the-clock power, a critical necessity in an age of intermittent renewables and volatile fuel markets. Their factory-built, modular design promises more predictable deployment schedules and cost control not seen in previous nuclear projects. Crucially, SMRs are the only scalable, dispatchable, zero-carbon resource capable of providing the continuous power demanded by artificial intelligence (AI) data centers and advanced manufacturing, securing their competitive economic advantage. Despite the promise of SMRs, challenges remain: specifically, waste disposal logistics, high upfront capital costs, and public skepticism inherited from decades of large-reactor projects.

Despite these challenges, they can be overcome, and Tennessee is well-positioned to do so.[6] The state is already a leader in nuclear energy provision. Nuclear power accounted for half of the state’s electricity generation in 2023, and remains a major source.[7] The state is also making history in next-generation power supply. In August 2025, Tennessee became the first state to be approved for an SMR. In partnership with the Tennessee Valley Authority (TVA) and Google, this SMR is the first of what is hopefully many in Google’s plan to purchase power from multiple SMRs.[8] In October, Radiant announced that it is developing its microreactor in Tennessee instead of Wyoming.[9] These developments continue a rich history of cutting-edge nuclear energy research in the state, which all began at the Oak Ridge National Laboratory (ORNL) in Oak Ridge, Tennessee. But they also highlight a dynamic unique to Tennessee between state and federal TVA and Nuclear Regulatory Commission (NRC) authority. Despite the strong federal authorities, the state holds a decisive lever for permitting, making state policy critical to success. Not only will these SMR advances benefit Tennesseans, but they will also serve as a proof of concept and benefit Americans across the country.

As the need for energy increases due to economic growth and technological progress, the question remains: will the government obstruct or facilitate industry partnerships to meet this demand and secure Tennessee’s and America’s energy leadership? The stakes are high, with other states actively competing to become energy production leaders. These factors highlight the need for a cohesive and enabling policy framework.

Energy Consumption in Context

Because policymakers frequently encounter power figures ranging from kilowatts to terawatts, clarifying these terms upfront ensures that later discussions of data center load and SMR generation are grounded and accurate. Without proper context, additional electrical load can seem alarming and the challenges insurmountable.

| Unit | Symbol | Power | Example |

Watt | W | 1 W | LED nightlight |

Kilowatt | kW | 1,000 W | Toaster or microwave (~1-2 kW) |

Megawatt | MW | 1,000,000 W | Small power plant or large data center (~50-100 MW) |

Gigawatt | GW | 1,000,000,000 W | Large power plant or a large city’s demand (~1-5 GW) |

Terawatt | TW | 1,000,000,000,000 W | Entire U.S. grid demand (~0.5-1 TW at any moment) |

While these national trends shape the overall energy landscape, their implications are particularly acute in Tennessee. The average residential electricity customer in the state uses approximately 1,154 kilowatt-hours per month, based on utility-reported sales and customer data.[10] One way to explain this number is that the average Tennessee home uses enough electricity each month to power a microwave running nonstop for 1,150 hours or 48 days. By comparison, a 50,000-square-foot commercial building might use ~3,100 kilowatt-hours per day, roughly 80 to 90 times the daily consumption of a single average household. At the large-city scale, Nashville Electric Service, which provides power to Metropolitan Nashville-Davidson County and parts of the surrounding counties, sold 12,198,000 megawatt-hours in 2025.[11] Another way of describing this number is in terawatt hours or 12.2 terawatt-hours.

Large amounts of energy are consumed every day, and in return, the Tennessee economy grows. Few sectors demonstrate this dynamic more than the recent increase in data center investment and construction.

What is a Data Center?

The term data center is widely used but often imprecise. It can describe a broad spectrum of facilities that store, process, and deliver digital information, ranging from small local server rooms to vast industrial-scale computing complexes. Although all data centers share the same core purpose—providing reliable computing infrastructure—their scale, ownership, and energy demands vary dramatically.

At the smallest end of the spectrum are enterprise or on-premises data centers, typically owned and operated by a single organization such as a hospital, university, or financial institution. These facilities handle private information systems, research databases, or internal communications. For example, Vanderbilt University’s IT system or HCA Healthcare’s patient-record servers would fall into this category. They are usually small to medium in size and draw tens of kilowatts of power.

Next are colocation facilities, which lease secure, climate-controlled space, power, and connectivity to multiple clients. These facilities support thousands of companies, from regional banks hosting secure transaction systems to mid-size e-commerce platforms backing up customer data. Operators such as Equinix and Digital Realty dominate this market segment. Their energy consumption typically ranges from hundreds of kilowatts to tens of megawatts.

The next category in size is cloud or hyperscale data centers, owned by major technology companies such as Amazon Web Services, Microsoft Azure, and Google Cloud. These sites power the everyday services consumers depend on—email, search, file storage, photo libraries, video streaming, and social-media feeds. When users upload photos to iCloud, watch Netflix, or use Google Docs, the computing work is performed within these facilities. These hyperscale centers are enormous in both size and power consumption, often consuming tens to hundreds of megawatts of electricity, which is comparable to the output of a small power plant.

Many companies run edge or micro data centers, which are small, distributed installations designed to reduce latency by placing computation close to end users. These connection points support content-delivery networks (ensuring fast video playback on YouTube and Netflix), 5G telecommunications, smart-traffic systems, and connected manufacturing equipment. Their electricity draw ranges from a few kilowatts to a few megawatts.

A rapidly expanding segment is AI and high-performance computing data centers, purpose-built for training artificial-intelligence models, running simulations, and supporting scientific or defense applications. These data centers are better described as supercomputers. They enable workloads such as chatbot conversations, model training, weather forecasting, genomics, and autonomous-vehicle development. These “AI centers” require very high power density, advanced cooling systems, and dedicated substations. Their energy use often reaches hundreds of megawatts, with new campuses projected at gigawatt-scale.

These particular data centers are driving the national conversation about build-out and energy needs. In a June 2025 report, Deloitte reported that AI data centers made up around 12 percent of power demand.[12] Data center power demand in 2025 is mainly driven by the kinds of data that enable typical e-commerce, website, cloud, and internet use. In the same study, however, Deloitte predicts that total data center power demand will rise to 176 gigawatts by 2035, with 123 gigawatts of that total going to AI-specific facilities. In a separate 2025 report by Grid Strategies, the authors estimate a lower load of 90 gigawatts by 2030 that is driven by data centers of all kinds.[13] With estimates showing increased energy needs, supply must be addressed before its too late. Given the approval and buildout timelines for SMRs, action is necessary now.

Together, these categories form a continuum of computing infrastructure that powers nearly every modern digital service. For analytical or policy purposes, it is important to recognize that “data center” does not denote a single type of facility but rather a diverse ecosystem differing sharply in physical scale, ownership, and energy footprint.

Understanding these distinctions is crucial for an accurate discussion of data center energy use, zoning, and grid impacts. Policymakers, utilities, and industry stakeholders must define the term precisely before concluding electricity demand, assessing environmental impact, or taking action on policy.

Data Center Energy Consumption in Tennessee

Nationwide, demand for data center development is exploding as AI use grows and more of life and computing move to the cloud. For example, as reported by the New York Times in an October 2025 article:

Google, Microsoft and Amazon, which are the three largest providers of cloud computing in the United States, said they did not have enough computing power to meet customer demand. That’s despite those three and Meta shelling out a combined $112 billion in just the last three months on capital expenditures, which included construction of data centers… ‘I thought we were going to catch up,’ Amy Hood, Microsoft’s finance chief, said in a call with investors on Wednesday. ‘We are not. Demand is increasing. It is not increasing in just one place. It is increasing across many places.’[14]

Globally, data centers accounted for around 1.5 percent of the world’s electricity consumption in 2024, or 415 terawatt-hours.[15] According to a report from Lawrence Berkeley National Laboratory on data center energy needs, “U.S. data center energy use has continued to grow at an increasing rate, reaching 176 terawatt-hours by 2023, representing 4.4 percent of total U.S. electricity consumption.”[16] The authors predict that data center electricity consumption could be equivalent to 6.7 percent to 12 percent of total U.S. energy needs by 2028.[17]

Despite this rapid expansion, it is important to note that data centers have simultaneously become dramatically more energy efficient. From 2010 to 2018, global data center electricity use grew by only ~6 percent even as compute instances increased 550 percent, thanks to significant improvements in server efficiency, storage density, virtualization, and cooling performance.[18] These gains mean that while total electricity demand is rising due to increases in computational workload, the growth would have been far larger without continuous efficiency improvements across the industry.

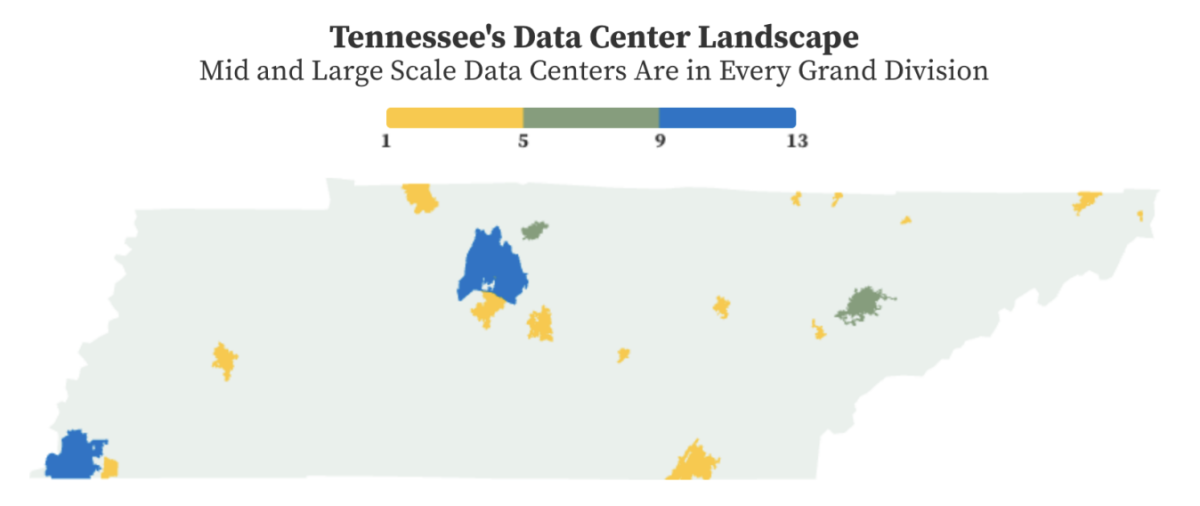

Tennessee is home to around 60 data centers.[19] This count excludes small server rooms but includes mid- and large-scale data centers such as xAI’s Colossus in Memphis and Meta’s data center in Gallatin.

While xAI has secured grid access of around 150 megawatts for the Colossus facility in Memphis, no official disclosure of total instantaneous power draw or annual energy consumption has been made public; independent analysts estimate a full-scale load in the 200-300 megawatts range.[20] Tennessee is unique in that it is home to national laboratories like ORNL, which houses the second fastest supercomputer in the world.[21] ORNL’s Frontier supercomputer consumes about 21 megawatts during normal operation.[22] In addition to the growing manufacturing and residential needs, the demand for data centers means electricity demand will likely not slow in the Volunteer State.

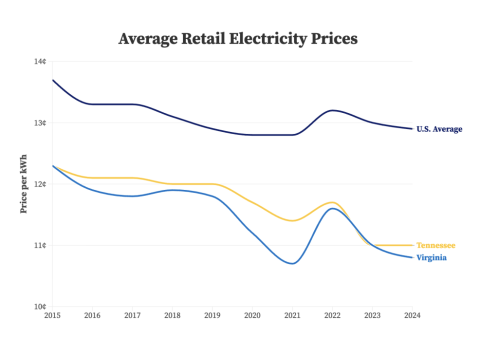

Given the scale of these new facilities, a common concern is whether additional load will increase retail rates. But the evidence tells a more nuanced story. While large data centers add substantial new electricity demand, research and utility case studies indicate that their impact on retail electricity prices is typically limited and context-dependent, rather than uniformly inflationary. For example, in Virginia, which is home to 10 times more data centers than Tennessee, a recent state-commissioned study reported that “… current rates appropriately allocate costs to the customers responsible for incurring them, including data center customers.”[23]

New data centers don’t have to mean higher bills for residents. As large scale users, this increased total amount of power sold can spread out the utility’s fixed costs over more kilowatt hours, making the entire system more efficient and affordable. The consistent, round-the-clock demand means utilities can confidently construct infrastructure knowing it will be used and paid for. Many large data center operators also reduce rate impacts by signing long-term power purchase agreements, paying for dedicated transmission upgrades, or directly financing new generation resources. The agreement between Google, Kairos, and the TVA is an excellent example.[25]

Overall, the net effect on retail customer prices in most documented cases is modestly beneficial. This is the headline finding of a landmark report published by the Lawrence Berkeley National Laboratory. Data shows that load growth, like that of proposed data centers, is one of the factors associated with electricity prices falling, not growing. As the authors explain, “Load growth at the state level has tended to depress retail electricity prices in recent years, by spreading fixed costs over greater load.”[26] The major reasons for increasing costs were inflation, renewable energy mandates, net energy metering rules for rooftop solar, and the upkeep of the poles and wires, especially relating to extreme weather events. This is a complicated area, however, and the authors of the report stress that load growth’s benefits are not guaranteed in all cases.27 Still, the findings suggest that additional load supporting investments in new generation and transmission infrastructure can benefit all customers.

Abundant, Reliable Energy

Tennessee must meet the needs of the new technological frontier. This is where advanced nuclear technologies, particularly SMRs, become central to Tennessee’s long-term strategy. The Volunteer State can meet all its new demands and more, making electricity more affordable for everyone. Even though the state consumes more than it produces, advances in technology, along with private sector investment driven by data center buildout, can help Tennessee close the gap.[28] Fortunately, leaders in Tennessee have recognized these trends and have taken positive steps to promote additional generation in the state. While power generation of any type involves trade-offs, the state’s diverse needs, geography, and growing demand show SMRs must be a critical part of the solution in the state.

An Overview of Nuclear Power

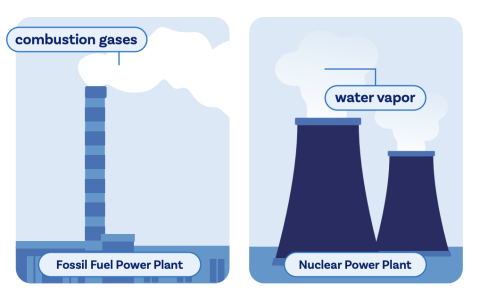

Nuclear power plants generate electricity by using heat from nuclear fission, the process of splitting uranium or plutonium atoms to release energy. The heat produces steam, which spins turbines to generate electricity. In this sense, it is much like a natural gas or coal fired plant, which burns natural gas or coal to create steam to turn a turbine that generates electricity. But nuclear plants simply release water vapor instead of combustion gases.

Nuclear power at the utility level has been at large plants such as Sequoyah and Watts Bar in Tennessee, which supply roughly half of the state’s electricity.[29] These facilities are examples of traditional pressurized water reactors, which typically produce over 1,000 megawatts each and operate continuously to meet baseload electricity demand.

Traditional reactors are large, complex systems that require extensive on-site construction and substantial cooling resources. They usually rely on large volumes of water drawn from rivers or lakes to manage heat, making them vulnerable during droughts or heatwaves. Due to technical and regulatory requirements, construction of these plants can take close to a decade or longer. The regulatory requirements, overseen by the NRC, are the primary reason nuclear power construction has mostly ceased in the U.S. As Josh Smith, an energy researcher at Pacific Legal Foundation, points out, “It took five years and $1 billion (adjusted to current dollars) to permit and build the Connecticut Yankee nuclear plant, which began operating on January 1, 1968. In contrast, Vogtle’s nuclear reactors in Georgia took 14 years just to build and cost more than $30 billion before the two reactors became operational in 2023 and 2024.”[30] Regulatory reform at the NRC is essential for America to meet its energy needs through nuclear power. These constraints point to the need for next-generation nuclear technologies that are more flexible, scalable, and cost-predictable.

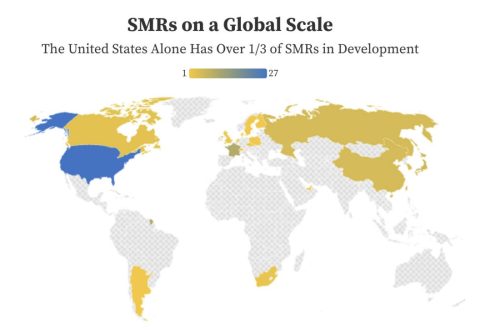

On the technical side, SMRs represent an exciting path forward. They are a new generation of nuclear technology designed for flexibility, safety, and efficiency. SMRs typically generate between 50 and 300 megawatts per module and can be factory-built, transported, and assembled on-site. This modular design significantly reduces construction time and capital costs. Instead of siting and building a large commercial facility like Watts Bar, SMRs are intended to be built in a factory, shipped, and then sited in a much smaller geographic footprint. According to the Nuclear Energy Agency at the Organisation for Economic Co-operation and Development, there are currently 74 SMRs under development around the world.[31]

Their design types are quite different from current, larger reactors. Many SMR designs use passive safety systems—such as natural circulation and gravity-fed cooling—that do not depend on active mechanical systems or operator intervention, enhancing safety. SMRs can also use less water or alternative coolants, allowing them to operate in locations unsuitable for large reactors. These characteristics work well for a state like Tennessee with mountainous and remote communities. SMRs provide grid-hardening flexibility, allowing power to be deployed near major load centers (such as data center complexes or industrial facilities) to reduce grid congestion and the need for new long-distance transmission lines.

Tennessee is leading the nation in SMR development. The Clinch River site near Oak Ridge, is being developed by TVA for a 300 megawatt SMR — the utility holds an early-site permit issued in 2019 and submitted a construction permit application in 2025, with commercial operation targeted around 2032. The project exemplifies the next wave of SMRs in the U.S. Notably, the Clinch River SMR employs a passive-safety light-water reactor design, meaning it uses proven water-cooled technology but relies on natural forces like gravity and convection—rather than powered pumps or operator action—to safely cool and shut down the reactor in emergencies.

Although SMRs offer Tennessee a promising source of reliable power, they introduce distinct waste-management risks and opportunities that the state should plan for early. Some SMR designs may generate higher volumes of spent fuel and activated structural materials per unit of electricity than today’s large reactors, driven by factors such as neutron leakage and alternative coolants.33 At the same time, Tennessee is uniquely positioned to manage these challenges: the Oak Ridge Reservation, including Y-12, ORNL, and the Environmental Management Waste Management Facility, already hosts one of the nation’s most experienced nuclear-materials ecosystems, providing technical expertise, workforce depth, and existing infrastructure for handling and characterizing complex waste streams.

Historically, commercial nuclear waste is extremely manageable. According to the U.S. Department of Energy, all commercial nuclear waste since the 1950s could be stored 30 feet deep on a football field, and it has been safely transported across the country for 50 years.[34] With thoughtful siting and planning between TVA, state regulators, and federal partners, Tennessee can mitigate SMR waste risks while leveraging its national nuclear assets to become a leader in next-generation fuel cycle management.

Ultimately, SMRs differ from traditional reactors in scale, safety, and deployment. While traditional reactors provide steady, large-scale baseload power, SMRs offer scalable and decentralized energy options that can support industrial facilities, remote regions, or energy-intensive uses such as data centers and military bases.[35]

Despite the exciting advances and government prioritization of SMRs, the Department of Energy expects the earliest deployments at the end of this decade and in the 2030s.[36] Increased private investment and smart changes to regulations could advance that timeline, but in the short term, SMRs are likely not the immediate energy solution. This does not, however, make action any less urgent. Rather, it makes action now all the more important. Because SMRs still have a multiyear development timeline, the predicted 123 gigawatt demand of 2035 means Tennessee must start approving new projects today. Delaying action by even two years ensures a capacity crisis. Such delays could mean companies resort to more costly alternatives or locate in other states where power is available. Without regulatory reform, residential ratepayers will not benefit from this generation. Changes now can be made to ensure new generation technologies benefit consumers and drive American economic growth.

Policy Recommendations

With these realities in mind, Tennessee’s policymakers have several clear opportunities to lead. Tennessee is the first state approved for an SMR. It is already leading the nation, and it can continue to do so. More generation capacity will be required for the state to meet the needs of new technologies and a growing economy. Indeed, as conveyed in the state Nuclear Energy Advisory Council report, the state’s energy leaders have understood this: “TVA’s [former] CEO Jeff Lyash has repeatedly stated in public that he is not interested in building a single SMR. He sees the need for 20 or more SMRs to meet the needs of the Tennessee Valley.”[37] Public policy reforms in Tennessee can ensure the market meets these demands for abundant energy.

Regulatory Reform First and Foremost

The best path forward for long-term economic growth and abundant energy generation is regulatory reform. Tax credits and subsidies provide short-term boosts and are attractive to industry. Still, they risk taxpayer dollars, inflate state budgets, and put the government in the business of picking winners and losers. Other, more pragmatic ideas without such downsides include the following:

- One state-wide interconnection standard for local power companies, ensuring reliable grid integration for new generators of energy.

- For the nuclear construction workforce, the state can ensure reciprocity for out-of-state nuclear certifications. For new talent, the state could fast track new certifications.

- Update water-use and environmental review for SMRs and advanced reactors. These updates could include a separate pathway for molten salt, gas-cooled, sodium-cooled, and microreactors; exemptions or accelerated review for ultra-low-water designs; and engineering reviews that match the technology, not legacy assumptions.

- With TVA, create a one-stop permitting approval office for state environmental approvals, state rights-of-way issues, Tennessee Department of Environment and Conservation permits, and local construction approvals.

- Allow islanded and self-contained grids outside of the existing utility system for industry and other users.38

- Expansions or additions of new generators at existing generation sites or at industrial sites can be fast-tracked through environmental review requirements. For example, adding an SMR at a site where another generator is at the end of its life, or where there is space for expansion, should be easier than building in a greenfield location.

- Tennessee should advocate for smart federal reforms to nuclear policy, such as better advanced reactor regulations and the end of the linear no-threshold modeling of radiation’s risks.

Establish a State Nuclear Coordinator

To ensure full readiness as technology advances and federal policy adapts, state policymakers should adopt the policies in the model Overturn Prohibitions & Establish a Nuclear Coordinator (OPEN) Act.[39] This model bill is designed to modernize state authority and clear away unnecessary red tape. It proposes to repeal outdated state or local moratoria and bans on the siting of nuclear facilities, removing longstanding barriers that have limited reactor construction. The model also calls for the creation of a dedicated State Nuclear Coordinator—a centralized official responsible for overseeing and streamlining nuclear permitting processes. To enhance efficiency, the OPEN Act envisions a one-stop state portal that consolidates all permitting and regulatory steps under a single system, with clearly defined timelines—typically within 180 days—for project approvals. Finally, it includes provisions to explicitly authorize and encourage the siting, development, and deployment of advanced reactors, including small modular and microreactors, under state regulatory leadership.

The language in the model bill could be amended to strike the appropriate balance between state authorities and those of the TVA. For example, the State Nuclear Coordinator position created in the bill would complement TVA’s federal nuclear authority by streamlining and aligning the state-side elements of nuclear project development (site readiness, incentives, workforce, supply chain, state permitting) and acting as the interface between TVA and Tennessee’s agencies. The state could direct the Coordinator to provide biannual or annual reports to the legislature on deployment progress. Finally, the permitting reforms in the bill language would ensure that all authorities controlled by the state are not unnecessary obstacles. It would do nothing to the TVA and NRC regulatory authorities. Of course, those agencies should take heed of what can be done within their jurisdictions to help Tennessee meet its energy needs with SMRs.

The Tennessee Nuclear Energy Advisory Council came to the same conclusion that motivated the development of the model OPEN Act. Much like other states, the Council found a “fragmented approach” that any nuclear-related industry would have to navigate. Based on a survey of the nuclear industry conducted by the Council, “…businesses find this fragmented approach challenging, and many expressed the need for a single, coordinated office that provides guidance on both regulatory and economic matters.”40 Recommendations 4-A-1 and 4-A-2 in the Council’s Final Report suggest the establishment of a Joint Office of Nuclear Advancement. The duties of that office could be included in a State Nuclear Coordinator position. This office would be a single point of contact for the nuclear industry and conduct an inventory of state nuclear approval processes to establish a “roadmap” for the state.

Make Tennessee Data Center Ready

Tennesseans have much to gain from the necessary build out of data centers.[41] To take advantage of this growth while protecting consumers, policymakers should:

- Streamline and standardize permitting, zoning, and siting processes to provide certainty and reduce delays while preserving local input.

- Align data center development with long-term energy and grid planning, with clear cost-allocation and interconnection rules that ensure large new loads pay for incremental infrastructure and do not shift costs or reliability risks onto existing ratepayers.

- Treat data centers as core economic infrastructure, integrating them into state and regional development strategies that expand the tax base, support workforce development, and fund public services.

- Avoid ad hoc or punitive regulations that single out data centers, instead adopting clear, technology-neutral policies that tie growth to grid investments, improved reliability, and durable, long-term benefits for Tennessee consumers.[42]

Leverage Private Capital

Venture capital and private investment in SMR development totals $3 billion in only four companies.[43] Therefore, recommendation 1.3 in the Tennessee Nuclear Energy Advisory Council Final Report is open-ended but offers important guidance: “The State should work with TVA to identify private investment capital aligned with TVA’s and the State’s long-term interests.”[44] As noted above, current private investment in data center growth and the willingness of technology companies to colocate or invest in generation capacity represent a unique opportunity to follow this guidance. Now is the time for officials and business leaders to lean into attracting investment partners. Making Tennessee the most attractive state to build and operate SMRs, through regulatory reforms instead of tax incentives, can lead these dollars to the Volunteer State.

Pending Opportunity for State Leadership in SMR Deployment

There is another critical legal effort that would allow states to oversee the regulation of SMRs, thus removing the NRC from the equation.[45] The lawsuit State of Texas et al. v. U.S. Nuclear Regulatory Commission challenges the NRC’s federal licensing authority over advanced and small modular reactors.[46] The plaintiffs include Texas, Utah, and Louisiana, as well as the Arizona State Legislature (acting through its legislative leadership). Several private SMR developers have also joined the suit: Last Energy, Inc., Deep Fission, Inc., and Valar Atomics, Inc. Together, these state and industry plaintiffs argue that the NRC has exceeded its statutory jurisdiction under the Atomic Energy Act, and because of their safety designs, that certain advanced or micro-reactor technologies should instead fall under state regulatory oversight. If authority is properly returned to the states for smaller reactors, Tennessee has much to gain, given TVA’s expertise, industry presence, policy posture, and technical expertise.

Align State Regulations with Federal Reforms

Fortunately, there is a national urgency for increased energy generation and a growing appetite to sweep away needless regulations that have delayed or prevented new nuclear power generation. The Trump administration released four executive orders directing agencies to streamline permitting processes, revisit guidance and rules, and expedite review of qualified test reactors, among other measures.[47] The administration has also welcomed industry investment in nuclear power buildout. President Trump has also prioritized and signed an executive order regarding data center buildout.48 State leaders should ensure Tennessee can take advantage of these federal opportunities.

If Tennessee aligns its policy with technological and economic trends, the state can not only meet its future energy needs but also set a national standard.

Conclusion

Tennessee stands at a critical juncture where accelerating technological advancement and a rapidly growing population are placing unprecedented demands on the state’s energy infrastructure. With a population projected to reach nearly eight million by 2040 and an economy increasingly dependent on electricity-intensive sectors like manufacturing, and opportunity for growth via data center development, the Volunteer State must secure an abundant and reliable power supply to maintain its economic momentum and leadership in the tech frontier.

Nuclear energy, particularly the deployment of SMRs, presents the most promising path forward. Tennessee is already a national leader, drawing nearly half of its total generation from existing nuclear plants and becoming the first state approved for an SMR at the Clinch River site. This legacy and proactive stance, supported by Governor Bill Lee and industry interest from partners like Google, positions the state perfectly to meet its future needs.

While SMR technology offers many benefits, its widespread deployment is still years away. Therefore, policy and regulatory action today is essential to ensure readiness. Tennessee policymakers should seize the unique opportunity presented by private-sector eagerness to invest in and construct new generation capacity. Furthermore, the state can streamline its internal processes to prepare for a nuclear abundant future. Adopting regulatory reforms like those in the OPEN Act would consolidate fragmented regulatory oversight, provide a single point of contact for industry, and ensure Tennessee remains at the forefront of the advanced nuclear movement.